Author: AMZA Capital

A construction loan usually starts with a good story. The borrower has a site under contract, a set of plans, a builder who says the numbers work, and a finished project that looks profitable on paper.

That is not enough to get funded.

Commercial real estate construction loans are underwritten less like ordinary property loans and more like a controlled release of risk. The lender is not just financing a building. It is financing months of execution before the building fully exists, before tenants move in, and before the final value can be proven in the real world.

That is why construction lenders can sound cautious, even when the project looks strong. They are asking a simple question from several different angles: if this project gets delayed, costs more than expected, leases slower than expected, or appraises differently than expected, does the deal still have a way to survive?

For borrowers, that mindset matters. A better construction loan request is not the one with the most optimistic pro forma. It is the one that makes the lender believe the sponsor knows where the project can go wrong and has already planned around it.

AMZA Capital works with real estate investors and developers on commercial financing requests, including ground-up construction, multifamily construction, heavy rehab, and related commercial real estate financing. This article explains how these loans are usually viewed, what lenders want to see, and how to prepare before asking for terms.

What commercial real estate construction loans actually finance

A commercial construction loan funds the building or major renovation of an income-producing or business-use property. That can include multifamily, mixed-use, retail, self-storage, industrial, office, or other commercial property types, depending on the lender and the deal.

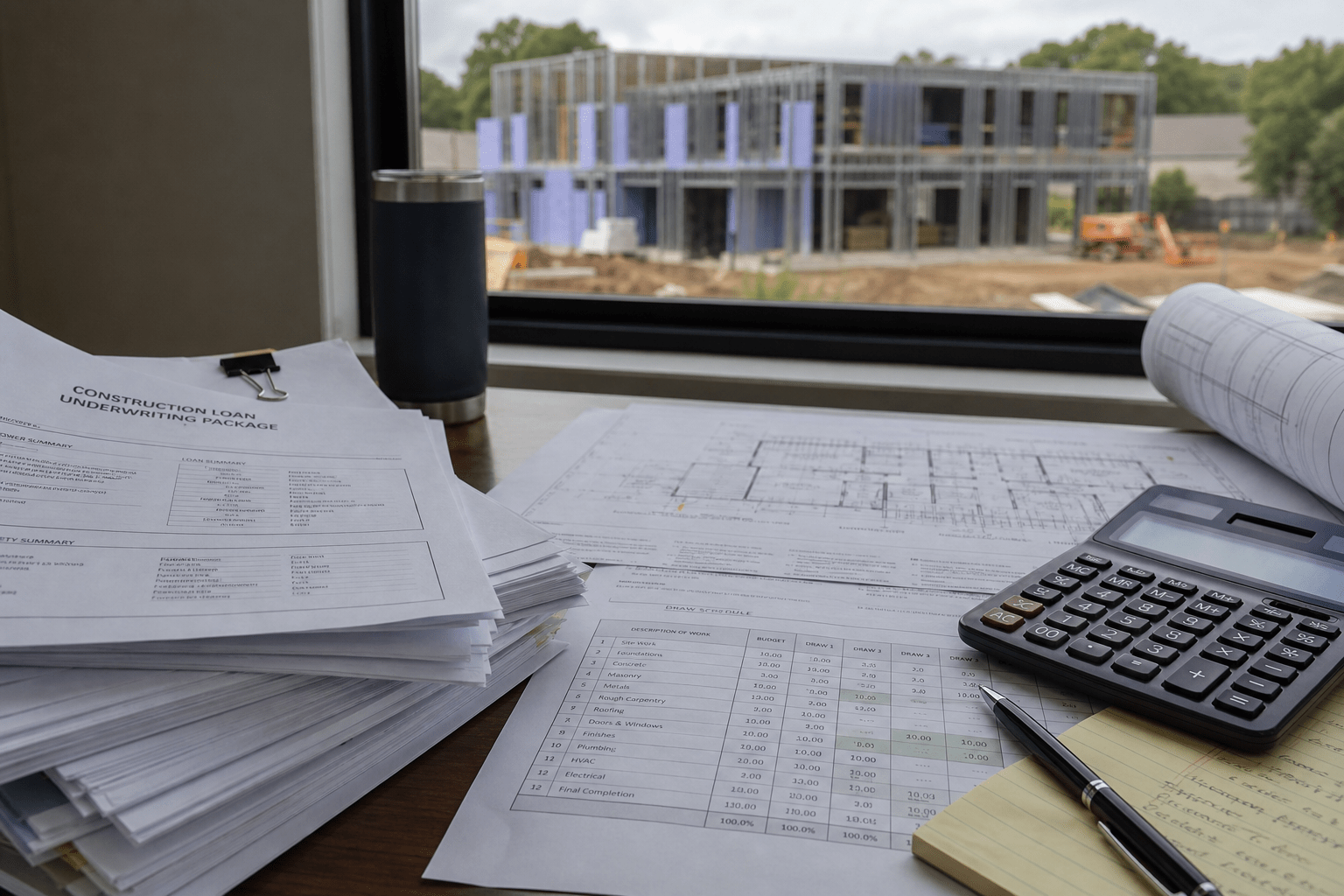

The loan may cover part of the land or acquisition cost, hard construction costs, soft costs, interest reserves, and sometimes a portion of closing costs. It usually does not work like a normal mortgage where all proceeds are released at closing. Instead, money is advanced in draws as work is completed.

That draw structure is the heart of construction lending. The lender wants to make sure the project is moving forward before more capital is released. A typical process involves inspections, draw requests, budget tracking, lien waivers, and periodic review of the remaining work.

For borrowers comparing options, AMZA's construction financing page is a useful starting point.

Why construction loans are harder than stabilized property loans

A stabilized property gives the lender more evidence. It has leases, rent history, operating expenses, occupancy, and market performance. Even if the file is imperfect, the building is already there.

A construction project asks the lender to believe in a future building.

That future depends on the sponsor, the general contractor, the budget, the permits, the market, and the exit strategy. A lender has to decide whether the finished value is realistic, whether the borrower can finish the project, and whether the final property can support a sale or refinance.

The loan is also exposed to timing. If a stabilized property takes 45 extra days to close, that may be annoying. If a construction project runs 45 days behind schedule, the borrower may burn through interest reserves, extend contractor costs, delay lease-up, and miss the best market window.

This is why construction lenders care so much about boring details. The boring details are where the risk hides.

What lenders check first

Commercial construction lenders do not all use the same program box, but the early review usually comes down to a handful of questions.

1. Is the sponsor qualified for this exact project?

Experience matters. Not vague real estate experience, but relevant experience.

A borrower who has owned rentals for ten years may still be new to ground-up development. A sponsor who has completed single-family flips may not be ready for a 30-unit multifamily build. A developer who has built in one city may still face surprises in another market with different permitting, labor, and inspection issues.

Lenders want to know what the borrower has built before, how recently, and at what size. If the sponsor is light on experience, the general contractor may need to carry more weight. In some structures, lender comfort may depend on the contractor being meaningfully tied to the project rather than casually named in a proposal.

That does not mean newer developers are automatically out. It does mean the file has to be honest about the gap. A smaller project, more borrower cash, stronger contractor, lower leverage, or better-documented exit can sometimes help offset limited experience.

2. Does the budget look real?

Construction budgets fail in two ways. Some are padded with guesses. Others are too clean.

A budget that looks too clean can be just as concerning as a budget that looks messy. Real projects have site work, utility questions, permit costs, contingency, insurance, carrying costs, and change orders. If the budget ignores those items, the lender assumes the borrower may be underestimating the job.

The lender will compare the budget to plans, contractor bids, local cost expectations, and the scope of work. If the borrower says the project can be built for a number that does not match the market, the loan may be cut, repriced, or declined.

A strong package shows where the numbers came from. It separates hard costs from soft costs. It includes contingency. It explains unusual savings instead of hoping the lender does not notice them.

3. Are permits and approvals realistic?

Permits can make or break the timing of a construction loan.

Some borrowers approach a lender too early, before the path to approval is clear. Others assume a permit is almost done because an architect or city contact sounded positive. Lenders tend to be more skeptical. They want to know what has already been approved, what is still pending, and whether there are zoning, environmental, utility, or entitlement issues that could delay the start.

A project that is truly shovel-ready is different from a project that is still working through approvals. Both may be financeable, but they are not the same risk.

4. Does the completed project have a believable value?

The completed value has to be more than a number in a spreadsheet.

For a multifamily project, the lender will look at achievable rents, comparable properties, operating expenses, vacancy assumptions, and market demand. For a retail or mixed-use project, tenant demand and lease assumptions matter. For self-storage or industrial, the lender may focus on local supply, absorption, and whether the property type has enough demand in that submarket.

Optimistic rent assumptions are one of the fastest ways to lose lender confidence. If the pro forma assumes top-of-market rents, fast lease-up, and no meaningful concessions, the rest of the file needs to support that view.

5. Is there enough borrower cash in the deal?

Construction loans are not built for borrowers who are trying to contribute as little as possible.

Even when leverage is available, the borrower usually needs liquidity for equity, closing costs, reserves, overruns, and delays. A lender may like the collateral and still decline the request if the borrower would be left with no cushion after closing.

This is where many good-looking projects get uncomfortable. The borrower can show a profitable finished project, but the lender wants to know what happens if the project costs more, takes longer, or needs additional capital before stabilization.

Construction liquidity is a serious underwriting point. As a rough planning concept, borrowers should expect lenders to look for meaningful liquidity relative to the loan size, not just enough cash to reach closing.

6. How does the loan get paid off?

Construction loans need a clean exit.

The exit might be a sale. It might be a refinance into permanent commercial debt. It might be a bridge-to-stabilization structure followed by takeout financing once leases and income are in place.

What does not work is a vague plan to “refinance later.” The lender wants to know what will change between closing and payoff. Will the building receive a certificate of occupancy? Will leases be signed? Will rents support debt service? Will the finished value create enough equity for a takeout loan? Is the borrower already talking to a permanent lender, or is the exit only a hope?

A good exit plan is specific. It does not have to be perfect, but it has to be grounded in the property and the market.

For broader market context, investors can review construction spending data from the U.S. Census Bureau. The point is not to chase a national headline. It is to remember that construction lending sits inside a real market for labor, materials, timing, and demand.

Vertical construction versus horizontal development

Borrowers sometimes use the phrase construction loan to cover everything from buying land to installing roads and utilities to building the final structure. Lenders often separate those risks.

Vertical construction means building the actual structure. Horizontal development usually means site work, roads, utilities, grading, subdivision work, and related pre-building improvements.

Many lenders are more comfortable with vertical construction than heavy horizontal development. Horizontal work can be harder to value, harder to exit, and more exposed to entitlement risk. If the project depends heavily on land development before the building can start, the borrower should expect more questions.

AMZA's current construction guidance reflects that distinction. For certain larger subdivision-style requests where the borrower is building multiple 1-4 unit properties, AMZA is mainly a vertical construction lender, with horizontal development limited within the overall structure. For a single 1-4 unit construction project, lot financing may be considered when AMZA is also financing the construction.

That detail will not matter to every commercial borrower, but the broader lesson does: be clear about what portion of the request funds land, site work, soft costs, and vertical construction. Do not make the lender reverse-engineer the budget.

Common reasons construction loan requests get declined

Construction loans often fall apart for practical reasons, not because the project is impossible.

Common problems include:

- Sponsor experience is too light for the size or complexity of the project

- The budget does not include enough contingency

- Permits or entitlements are not far enough along

- Borrower liquidity is too thin after closing

- The completed value depends on aggressive rent or sale assumptions

- The market is too rural or thin for the lender's program

- The requested leverage leaves no room for delays or cost overruns

- The exit plan is not specific enough

- The general contractor is not proven for the scope of work

The best borrowers do not hide these issues. They address them before the lender asks.

How AMZA Capital approaches construction financing requests

AMZA starts by trying to understand the project as a whole: sponsor, property, budget, approvals, contractor, timeline, market, and exit.

For ground-up construction, borrower and builder experience matter. Lenders want to see comparable recent experience when possible. If the borrower has not completed a similar project before, an experienced general contractor can help, especially when that contractor is clearly tied to the project and accountable for the work. Multifamily ground-up and heavy rehab requests are reviewed deal by deal, with stronger files usually showing experienced sponsors, realistic budgets, and a credible exit plan.

AMZA also screens for location, property type, and loan structure before spending a borrower's time on a full package. Commercial, multifamily, and 1-4 unit residential construction requests are not always treated the same way, and availability can vary by state and program. If a request cannot be placed as structured, the better answer is to identify that early and look for a cleaner path rather than forcing the file into the wrong box.

Those details are not meant to make the process rigid. They are meant to prevent a borrower from spending time on a request that cannot be placed as structured.

What to prepare before requesting terms

A construction loan request does not need to be perfect before a first conversation, but it should be organized enough for a lender to give useful feedback.

Prepare as much of this as possible:

- Property address and project summary

- Current site status and ownership or purchase terms

- Plans, renderings, or scope of work

- Construction budget with hard costs, soft costs, and contingency

- General contractor information

- Permits, approvals, or current permit status

- Project timeline and draw schedule

- Borrower experience summary

- Liquidity available for equity, reserves, and overruns

- Completed value support, including comps or rent assumptions

- Exit plan: sale, refinance, lease-up, or takeout financing

If the request is still early, say that plainly. A lender can often give a preliminary read before every document is complete. But the more uncertainty in the file, the more conservative the feedback will be.

If your project involves broader commercial property financing rather than construction specifically, AMZA's commercial real estate financing page may be the better starting point.

A better way to ask for a construction loan

The strongest construction loan requests do not try to make the project look effortless. They make the project look controlled.

That means the borrower can explain the risks, the budget has room for reality, the contractor makes sense, the approvals are understood, and the exit is specific enough to underwrite.

A lender does not need every construction project to be simple. Very few are. But the lender does need to believe the borrower is not discovering the hard parts for the first time after closing.

For a free, no-obligation quote, fill in and submit one of AMZA Capital's quote forms. It only takes a minute.

START WITH AMZA CAPITAL’S FREE QUOTE PAGE.

For construction-specific financing, review AMZA's construction financing page.

This content is provided for informational purposes only and does not constitute financial, legal, or investment advice. AMZA Capital is a licensed mortgage lender (CA DFPI 60DBO 86104 | NMLS 2262631). Actual loan terms, rates, and availability vary. Consult a licensed financial professional before making investment decisions.

{kind=link}